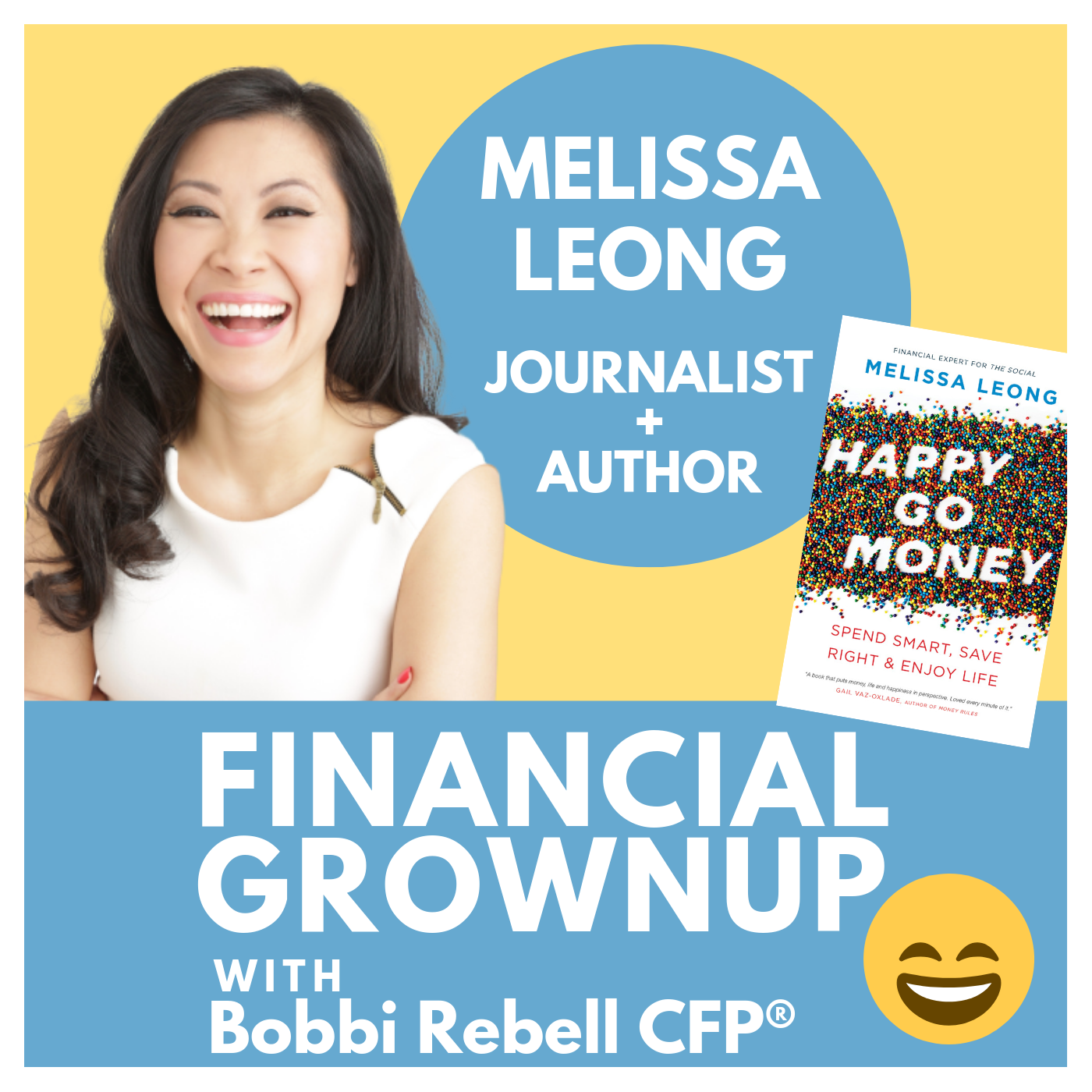

Happy Go Money author Melissa Leong shares the story of how her teen novels were rejected by mainstream publishers, but went on to sell over 70,000 copies after she decided to take control of her own career. Plus everyday social media tips to be happier no matter how much money you have or don’t have.

“You can’t wait around to make the perfect amount of money. You can’t wait around for your boss to give you that raise for you to be happy.”

Melissa’s Money Story:

I tried to shop this around. It's a vampire series, during the time ... Well, it was the tail end of Twilight, so no publisher wanted another vampire book. So I got a lot of no’s, in which case I was faced with this decision of, what is my dream worth? I want to get this done, so what am I willing to invest in myself? So I created a budget of how much I would spend on, pay a designer to create a cover, to publish it myself, to put it out into the world.

I self-published it, and yes, it turned out, in more ways than one, to be a great, great experience, something that I consider a success in my life. Something that I could check off my bucket list. And I still get the occasional check in the mail, even though I don't do all that much work publicizing it. I did make my money back and then some, and it was basically a great gift that I could give to myself, just in terms of learning that I could build a brand, make money for myself outside of a salary, and take those tools and make more money in another career.

Bobbi Rebell:

Tell us more about the journey. Did you write it first, and then you went to different publishers? How did it actually work? And how did the economics change between, if you had gotten a deal with a traditional publisher versus your own situation where you were self-publishing? What did that actually involve from a business and an economic standpoint, and a marketing standpoint?

Melissa Leong:

I think people don't realize that when you go and you create any product, you are entering into a business. You're your own business. You're your own publisher. I learned so much about being my own marketing department, my own publishing, and quality control, and PR, and that all requires resources, time and money. So yeah, I didn't have a publisher to push my books, but because I was doing everything myself, I had full control, and I had a huge percentage of the cut of sales. A traditional publisher might give you 7% off of the book selling price, but say you publish through Amazon, you get 70%, depending on what you price the book at. That was really rewarding.

Bobbi Rebell:

I realize we were talking about PR for the book. We didn't say what the book title was, and where people can get it. We should say that, right?

Melissa Leong:

Yes. It's still on Amazon. The first book is called What Kills Me, and the second is I Am Forever. It's a teen adventure novel. It's based on a vampire story.

“Mute the people on social media who make you feel bad about yourself”

Melissa’s Money Lesson:

The same lesson that I have when it comes to happiness. I think we sit around waiting for external factors to fulfill us, and that's not how life will serve you best. You can't wait around to make the perfect amount of money. You can't wait around for your boss to give you that raise, for you to be happy. Happiness is for you to fulfill for yourself. It's the same thing with any of your goals or your dreams. They all seem lofty, and they all seem huge in the beginning, but you have to take that first step. You turn on the heat, and if you turn off the heat before the water boils, the water will never boil. You just have to keep going. You break everything down into some sort of small, bite-sized goal, like writing a 60,000-word book in six months. That was my goal, and I thought, "That is ridiculous. How am I going to do that?"

Well, I broke it down to the smallest thing. Every single day, five days a week, I have to write 500 words. There you go. If, by the end of the day, I haven't written 500 words of something for this novel, then I didn't feel good. I also had a partner who I could check in with, and say, "I met my goal today. Yay. Somebody keep me accountable." It was something very tangible to do in a very short period of time.

“I was faced with this decision. What is my dream worth? I want to get this done and so what am I willing to invest in myself”

Melissa’s Money Tip:

There is a study that shows that if you live beside somebody who's won the lottery, you are more apt to go bankrupt, because you're also spending on tangible, visible assets, even though you have not won any money. It is something that we beat ourselves up for, but it's something that you can control. You can put a tracker on your phone to see how much time you spend on social media. You can mute the people on social media who make you feel kind of jealous, who make you feel bad about yourself, who don't share your values. You can fill your feed with things that are uplifting, things that inspire you.

If you find yourself comparing yourself to other people, then choose what specific attributes that they have, that you admire. Don't admire somebody because they're rich. Admire them because they have some sort of tenacity, or some sort of perseverance quality that you think that you would like more of in your own life.

Bobbi’s Financial grownup tips:

Financial Grownup tip number one:

Inventory your stuff. We're not saying to do a Kon-Mari, reference to Marie Kondo, who is known for Tidying Up. Just know what you own, so you can make a decision about whether you want to own more. At least know what you have, so you don't make buying mistakes. So, for example, you don't buy something that you already have five of, you just didn't know where they were. And let's be honest, we've all done that. Make sure you know where your stuff is, so it's there for you when you need it.

Financial Grownup tip number two:

Again from Melissa's book, Happy Go Money: Delete your credit card info from the browser on your computer, your phone, iPad, whatever you use to shop, so you have to manually enter it each time you want to buy something. What I love about this advice is that it's not about buying something, whether you need it or just want it. That's okay. It is about creating a speed bump so you have to slow down and think about the decision, and make it a thoughtful one, and it's okay to buy things.

Episode Links:

Blinkist - The app I’m loving right now. Please use our link to support the show and get a free trial.

Melissa's book Happy Go Money

Melissa’s website - www.MelissaLeong.com

Follow Melissa!

Instagram - @LisLeong

LinkedIn - @MelissaWLeong

Twitter - @LisLeong

Facebook - @Melissa.W.Leong

Some of the links in this post are affiliate links. This means if you click on the link and purchase the item, I will receive an affiliate commission at no extra cost to you. All opinions remain my own.

Happy Go Money author Melissa Leong shares the story of how her teen novels were rejected by mainstream publishers, but went on to sell over 70,000 copies after she decided to take control of her own career. Plus everyday social media tips to be happier no matter how much money you have or don’t have. In this Financial Grownup podcast episode you’ll learn the things you can do to create your happiness. #Happiness #Author